(E-)Mobility news

Everything you need to know about the 2023 fleet tax

At the end of November 2021, the government published a new law to make our mobility fiscally and socially greener. This law contains changes regarding the tax deductibility of company cars and charging stations, as well as updates in the mobility budget and the CO₂ contribution for company cars.

In the middle of last year, we already shared a first overview of the main tax changes in the law.

In this article, we provide an update with a focus on the changes for company cars and charging stations. Find out everything you need to know about the fleet tax laws and charging stations by 2023.

Calculation of the deductibility

The new tax system aims to make vehicles with combustion engines (diesel, petrol and hybrid vehicles) less attractive and phase out the deductibility of electric vehicles so they will eventually be taxed in the same way as wages.

The deductibility is calculated according to the formula below. It takes into account the CO₂ emissions and the type of vehicle propulsion.

120 % — (0,5 x fuel coefficient x CO₂ g/km)

CO₂ emissions are expressed in g/km. The type of propulsion is represented by a fuel coefficient. This will be adjusted progressively over the years, taking into account the lowest (50%) and highest (100%) deduction percentage possible.

For the 2023 calculation, the coefficient is as follows:

● 1 for diesel and plug-in hybrid diesel.

● 0.95 for petrol, hybrid, and plug-in hybrid petrol.

● 0.90 for natural gas vehicles up to a maximum of 11 fiscal HP.

Diesel, petrol, and hybrid vehicles

Diesel, petrol, and hybrid vehicles are all CO₂-emitting vehicles. The rules below apply to these types of vehicles:

Ordered between 01/01/22 and 30/06/23

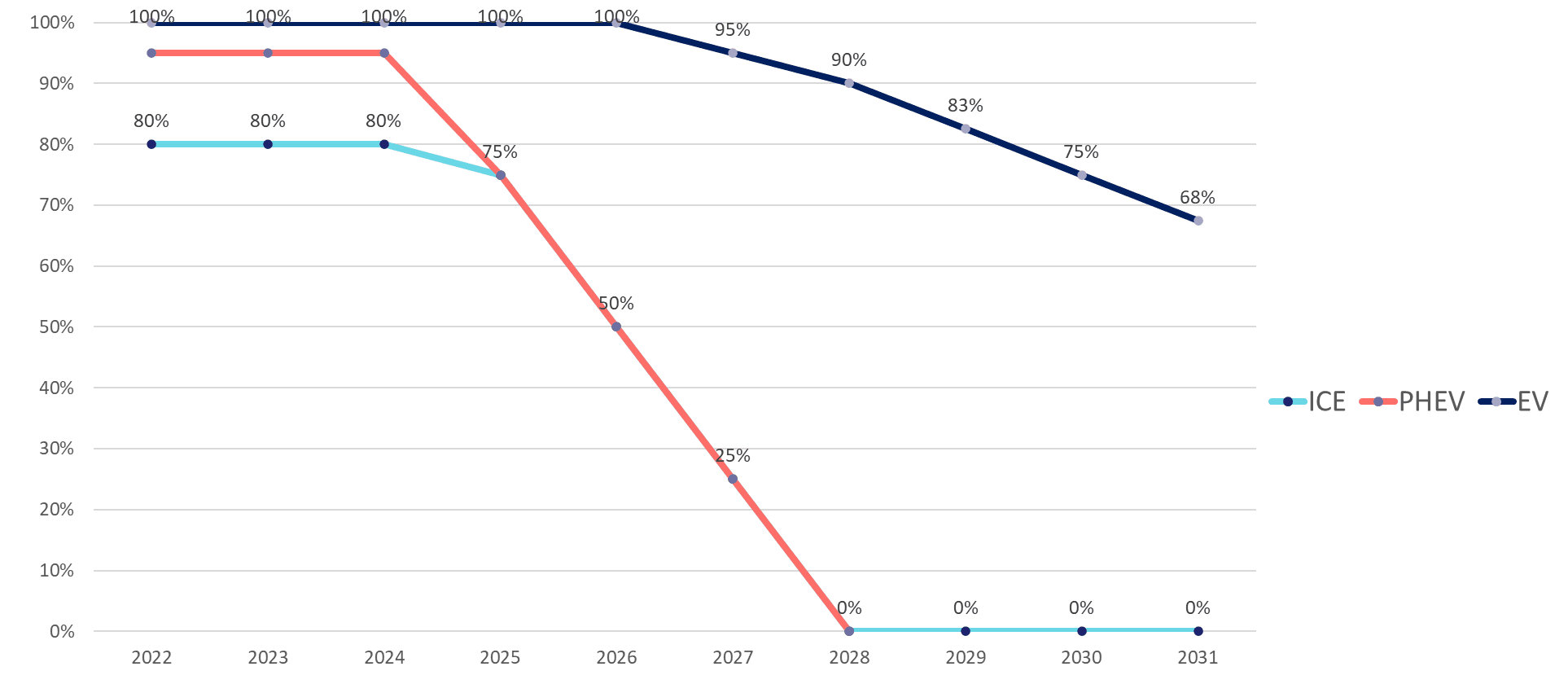

All CO₂-emitting vehicles ordered between 1 January 2022 and 30 June 2023 benefit from a maximum deductibility of 100% and a minimum deductibility of 50% until 2031.

Vehicles with CO₂ emissions above 200 g/km benefit from a minimum deductibility of 40% (penalty rate).

For PHEVs (plug-in hybrids) ordered from 1 January 2023, fuel costs (diesel or petrol) are deductible up to 50% until 31 December 2026.

Ordered between 01/07/23 and 31/12/25

All CO₂-emitting vehicles ordered between 1 July 2023 and 31 December 2025 benefit from a maximum deductibility of 100% and a minimum deductibility of 50% until 2024.

After 2024, the maximum deductibility will decrease by 25% each year to reach 0% in 2028. The minimum deductibility already disappears completely after 2024 (0% from 2025).

A minimum deductibility of 40% (penalty rate) also applies to these vehicles (until 2024) if their CO₂ emissions exceed 200 g/km.

Ordered after 01/01/26

After 1 January 2026, no more CO₂-emitting vehicles will be tax deductible. In other words, from 2026 onwards, it will NO LONGER be fiscally attractive to order diesel, petrol, or hybrid company cars.

Electric vehicles

Electric cars do not emit CO₂ and are considered zero-emission vehicles. The following rules apply to these vehicles:

Ordered before 01/01/27

Electric vehicles ordered before 1 January 2027 remain 100% deductible until 2031.

It is important to note that this 100% deductibility remains in place until the legal ownership of an electric vehicle is transferred.

Ordered from 01/01/27

For electric vehicles ordered on or after 1 January 2027, the deductibility will be progressively reduced each year until it reaches a minimum of 67.5% in 2031.

The table below summarises the maximum deduction rates up to 2031 for electric vehicles (EVs), plug-in hybrids (PHEVs) and internal combustion engine (ICE) vehicles.

Charging stations deductibility

Of course, the electric transition of our mobility requires the establishment of the necessary charging infrastructure. Therefore, the government has made it more attractive for companies to invest in (semi-) public charging stations.

This way, the costs for the installation of charging stations are 200% deductible until 31 March 2023 and 150% deductible from 1 April 2023 to 31 August 2024.

For companies to benefit from this increased cost deduction, their charging stations must meet the following conditions:

- Charging stations are smart stations that allow an energy management system to control charging time and power.

- Charging stations are located in publicly accessible places (e.g. car parks or freely accessible places).

- Charging stations are accessible/usable by third parties for at least 10 hours per day.

- The location and availability of charging stations can be checked by registering with FPS Finance or on the eafo.eu website.

- Charging stations may NOT have been purchased through operational leasing.

Changes to the CO₂ contribution

Besides the changes in terms of the tax deductibility of company vehicles and charging points, the new legislation of the government also includes a change in the calculation of the CO₂ contribution for company vehicles.

More information on the new fleet taxation

Would you like to know more about the new fleet taxation? Check out our own flyer and the updated one-pager from our Mobia colleagues at Febiac below.

Learn more about electric driving and leasing

Do you want to continue to benefit from tax advantages for your company cars? In this case, it is essential that you start thinking about the electric transition of your fleet now.

At Alphabet, we can be your partner for a smooth transition and integration of electric vehicles. From personal advice on the right vehicles to efficient leasing and driving, we will guide and support you from A to Z.

Contact us without obligation for more information.